The tide is turning for investments considered purely on financial terms, as new research confirms the rising importance of ESG to dealmakers.

New research from Baker Tilly and Acuris confirms the rising importance of ESG to dealmakers.

When it comes to the ability of a business to live up to its values, there’s nothing like a crisis to sharpen the mind.

It explains why the treatment of employees, behaviour within the community – even outward demonstrations of support for public health and science — have become pressure points for business over the past year.

Between the pandemic, lockdowns and furloughs, the urgent focus on climate change, and a mood of social upheaval and protest around the globe, businesses have been expected to live up to the PR spin of being good corporate citizens.

Indeed, the past year may have marked a turning point for the importance of ESG (or environmental, social and governance issues) both for the business community and for the customers and markets they hope to engage.

“The tide has turned for businesses perceived as negative for their communities, who shun good governance or have track records of poor social outcomes.”

– Michael Sonego

“It’s been a traumatic year for business right around the globe, and there is naturally increased scrutiny on how they have managed,” says Michael Sonego, who leads Baker Tilly’s Corporate Finance strategic group.

“We have seen businesses that have criticised lockdowns boycotted by customers in return. We have seen companies that treat their employees badly struggle to re-engage staff. Where there have been publicised cases of environmental damage or corporate misbehaviour, the reputation hit has been huge.

“These issues not only damage the public perception and bottom line of a business, but they make a business far less attractive to investors or buyers looking at M&A.”

The scale of the shift is apparent in new research from Baker Tilly and Acuris, which looks at the impact of ESG issues both on mergers and acquisitions and on investment decisions.

It confirms the rising importance of ESG to consumers — with 90% saying they had become more concerned about these issues — which is having a knock-on effect on investors conscious of their own corporate social reputations.

“Consumers buy on belief: they want to know the business or brand they are engaging with has treated its people well, that it is not damaging the environment, that it is working appropriately for their communities,” Mr Sonego says.

“We have seen this become a pressing issue for businesses in terms of their behaviour when engaging with their people, customers and the environment, so it is unsurprising that ESG is top of mind for investors and shareholders.

“The tide has turned for businesses perceived as negative for their communities, who shun good governance or have track records of poor social outcomes. They are not only going to get punished by consumers and staff but by investors as well.”

Dealbreakers and opportunity makers

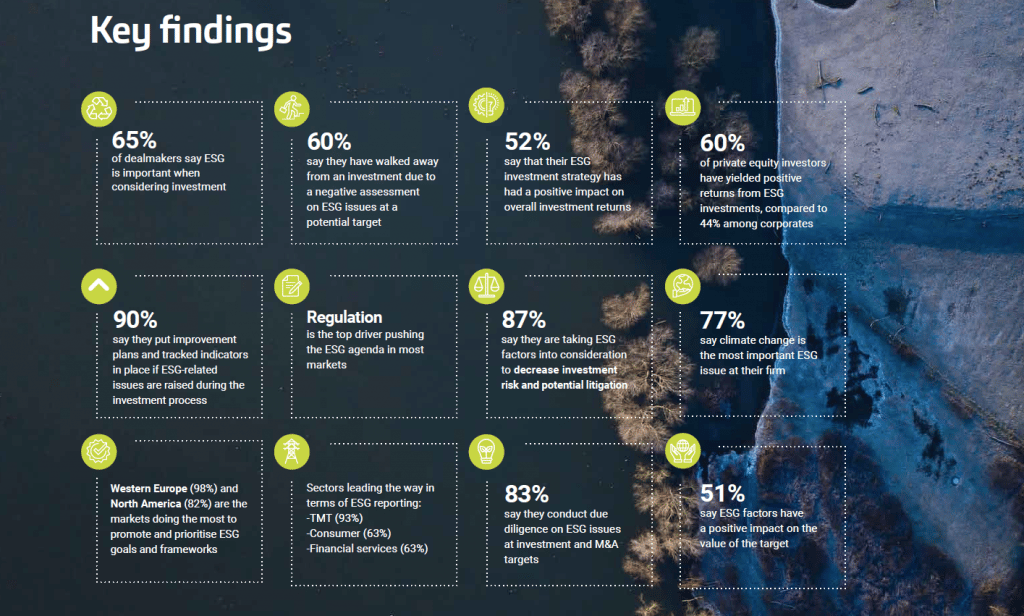

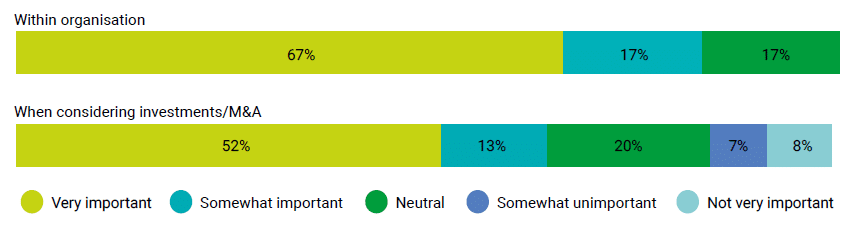

The report, which looked at the views of 60 dealmakers worldwide, finds ESG is more critical than ever in weighing up M&A and investment targets, with 65% of respondents considering it an important part of the investment strategy.

While regulation and outside pressure is responsible for some of that awareness, 84% of respondents say the issue also matters to their organisation, suggesting the tide is turning for investments considered purely on financial terms.

“Dealmakers see these issues as having a value to their own organisations and reputation, and that is shaping the way they approach potential transactions,” Mr Sonego says.

“Reputation and brand management are key drivers and, if an M&A target risks harming the bidder’s reputation, that has implications for the bidder’s key stakeholders, including consumers and their own employees.

“Dealmakers are acutely aware that bad ESG is hard to contain.”

Walk away or bargain down

“It can be tempting to think about ESG investing as being driven by the heart not the head, but our survey shows that’s just not the case.”

– Julie Haeflinger

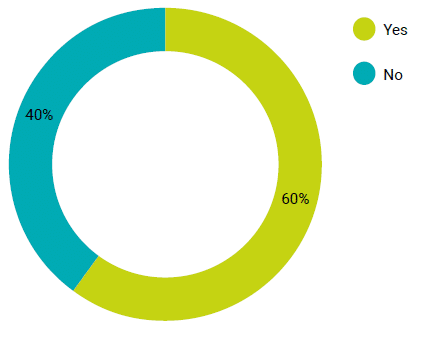

The Baker Tilly report found 60% of dealmakers reported walking away from a deal due to a negative assessment on ESG issues at the target.

And for those who did not, other motivations emerged.

Some saw the ESG issues as a lever to negotiate a better price for the target while others, particularly private equity investors, saw an opportunity to turn around poor ESG performance to generate better returns.

Some 63% of PE investors say they put an ESG improvement plan in place when they identify ESG issues in an acquisition, perhaps explaining why 60% of PE investors say their ESG investment strategy produces positive returns.

Among corporates — who are less likely to have a formal improvement plan in place — only 44% say they have seen positive returns while 17% say it is too early to know.

“It can be tempting to think about ESG investing as being driven by the heart not the head, but our survey shows that’s just not the case,” says Julie Haeflinger, Executive Director, Corporate Finance at Baker Tilly Strego.

“A high proportion of dealmakers have seen consistently better returns for investments with a strong ESG profile, and those who say they have not yet seen those returns are likely to be early in the investment cycle. Very few report a worse performance for an ESG investment over one where the environmental, social or governance profile is less favourable.”

As one partner in a German PE firm put it: “Our ESG objectives have certainly improved our returns – in the midst of the Covid-19 crisis, ESG has become the major subject discussed with stakeholders.”

A Canadian PE CEO explains the relationship by looking at the associated governance and structures of targets with strong ESG track records: “The performance of companies is related to their ESG standards; those with suitable credentials have fewer problems.”

Social conscience pricked by risk and regulation

While ESG issues won’t sink every deal, understanding the drivers behind the buyer’s ESG investment is key to assessing the level of risk they are prepared to take on.

In many cases, the key driver for investing in companies with a strong ESG record is to combat the threat of regulation, amid growing global demands for more sustainable investment.

PE and corporate investors are increasingly required to demonstrate performance that aligns with environmental goals on issues such as climate change, sustainable land and water use, and protection of biodiversity.

On social issues, there’s a renewed focus on human rights and labour standards, secure and sustainable employment, and avoidance of sweatshops, forced labour or modern slavery.

“Going forward, we expect both business and the investors targeting them to be more overt in pushing environmental credentials.”

On the governance front, tax avoidance, corruption, executive pay and even customer data security are all on the agenda for improvement.

Indeed, the United Nations’ Principles for Responsible Investment documents more than 730 regulatory revisions in the world’s 50 largest economies that require or encourage investors to consider long-term value considerations such as ESG factors.

Mr Sonego says these issues will only grow in importance, so investors are looking to the regulation horizon when weighing up targets.

“When we look at the increasing level of regulation in most countries around things such as the sale of cars with internal combustion engines, or the use of single-use plastics, our take is that a poor track record of environmental performance is only going to increase as a deterrent for deals,” he says.

“Going forward, we expect both business and the investors targeting them to be more overt in pushing environmental credentials, whether that’s a reduction of emissions, the use of renewable power, a change to lower-carbon supply chains or other measures that demonstrate the company understands the importance of the E in ESG.”

A second key driver is legal risk — including class actions against companies for alleged ESG abuses by consumers and shareholders.

In the US, 2020 was a bumper year for class actions relating to workplace issues, including the $310 million settlement of shareholder action against Google’s parent company over claims of executive sexual misconduct and the $14 million settled action against retailer Walmart claiming pregnancy discrimination.

“If a company has a legacy of poor treatment of employees, contractors, customers, stakeholders or the community, the risks quickly start to add up.”

– Julie Haeflinger

Out of more than 1500 class actions on wage and employment issues, 61 related to cases where employees felt unsafe in having to work during the pandemic.

In Australia, a group of eight teenagers has taken class action against the Federal Government over a decision to expand a coal mine, arguing it has a duty of care not to exacerbate the risks of climate change.

In Germany, a proposed supply chain due diligence law will introduce new legal penalties for large companies that do not act against human rights violations or environmental damage within their supply chains.

“If a company has a legacy of poor treatment of employees, contractors, customers, stakeholders or the community, the risks quickly start to add up,” Ms Haeflinger says.

“Whether it is wage-theft among low-paid workers or allegations of modern slavery in the supply chain, or just a senior leader with a reputation for appalling office conduct, the social risk of bad behaviour is now too expensive for a bidder to ignore.”

Dealmakers want to know not only that the company has avoided legal action to date but also that no sleeper issues will emerge.

“Due diligence in this area is complex and time consuming, but 83% of dealmakers now want ESG discussed in the earliest stages of a deal before negotiations progress,” Mr Sonego says.

“Once those issues are clear, more than half say they have changed the valuation of a target; 33% increasing their valuation and 18% downgrading it.

“Bidders want some certainty that are not buying a law suit waiting to happen, and strong ESG performance gives them comfort that won’t be the case.”

Related content